From flip to hold: 20+ years of PE investment in B2B events

Private Equity has been investing in the events industry for longer than the 20+ years I have been in it as an Operator, Executive (ITE / Hyve / Tarsus), and now Entrepreneur/Advisor. The model has been fairly consistent: buy good assets, back great teams, professionalise the business, unlock M&A, scale the asset, and exit. But are we now reaching a different point in the cycle? Are the best event platforms becoming assets PE wants to keep compounding, rather than sell on?

The CloserStill deal certainly looked that way. The reported £1.35bn valuation was eye-catching, but the real signal was quieter: Providence stayed in and brought in its co-investor from Hyve, Searchlight. Then Apollo announced Emerald + Questex. And now Hyve itself has reportedly been sold to Hellman & Friedman for about $1.8bn.

Premium event platforms are becoming institutional assets. Some are being held and recapitalised. Some are being combined into larger platforms. Some are still being flipped, but at a very different scale.

Events PE M&A deal valuations by year

Total disclosed / estimated transaction values by year, with a 3-deal rolling average. Values are approximate GBP equivalents and mix reported transaction values, enterprise values and valuations where only those figures are publicly available.

Notes: bars aggregate annual totals. The moving average is calculated on the underlying deal sequence and shown once per year using the year-end value. Includes Questex / MidOcean at reported c.$180m, converted to c.£140m for charting; Hanson Wade / Graphite at reported £102m; and Nineteen / Phoenix at reported c.£10m. Excludes undisclosed transactions, non-valued platform formations, Emerald IPO gross proceeds, Canon / UBM, Mack Brooks / Reed, and Informa / UBM as a strategic mega-deal outlier. Apollo / Emerald + Questex is treated as closed for this chart and uses an analytical estimate of c.$2.0bn / c.£1.5bn. Hyve / H&F is treated as closed at c.$1.8bn / c.£1.35bn.

The chart above shows a clear re-rating of the sector. The annual totals are uneven because the dataset depends on disclosed or estimated values, but the direction is hard to miss: early transactions were often sub-£200m, with occasional spikes, while the post-2013 period increasingly features platform-scale deals. By 2019, 2023 and 2026, the annual totals are being driven by larger, more institutional transactions: Tarsus, Hyve, Easyfairs, Nineteen, CloserStill, Emerald+Questex, and now Hyve again. The important point is: the ceiling has moved. Events have gone from mid-market M&A territory to a market where £500m–£1bn+ platform valuations are credible when the asset has scale, vertical strength, rebook, data, M&A potential and management depth.

Now let’s have a look at the extended data behind this chart:

(I wanted to build this table for a very long time, this’ll take a few scrolls)

| # | Date | Asset | Buyer / investor | Seller / prior owner | Deal type | Reported Value | Notes |

|---|---|---|---|---|---|---|---|

| 1 | Oct 2004 | Clarion Events | HgCapital + management | Earls Court & Olympia | MBO | £45m | Starting point of Clarion’s PE journey. |

| 2 | Dec 2006 | Incisive Media | Apax + management | Public shareholders | Take private and MBO | c. £199m | Early Apax-backed B2B media/events take-private. |

| 3 | Dec 2007 / Mar 2008 | Emap B2B | Guardian Media Group + Apax | Emap plc | Break-up acquisition | c. £1bn; some references cite c. £1.3bn | Major B2B publishing + exhibitions platform transaction. |

| 4 | Feb 2008 | Clarion Events | VSS | HgCapital | PE-to-PE sale | £120.5m | Clarion’s first major PE-to-PE handoff; value rose from £45m MBO to £120.5m sale. |

| 5 | 2008 | Comexposium formation | CCIR + Unibail-Rodamco | Comexpo + Exposium merger | Platform formation | n/a — platform formation | Created the platform Charterhouse later bought into. |

| 6 | Sep 2010 | Canon Communications | UBM | Spectrum Equity + Apprise Media | Strategic acquisition from PE-backed owner | $287m / c. £185m | PE-backed vertical media/events platform exits to strategic buyer UBM. |

| 7 | Aug 2011 | GLM / George Little Management | Providence Equity | DMGT | Acquisition | £106m / $173m | Providence’s early US trade-show move before Clarion, CloserStill and Hyve. |

| 8 | Jun 2013 | Nielsen Expositions / Emerald | Onex | Nielsen Holdings affiliate | Acquisition | $950m cash consideration | Onex buys one of the largest US B2B tradeshow platforms. |

| 9 | Jun 2014 | CloserStill Media | Phoenix Equity Partners | NVM Private Equity / existing shareholders | Partial sale / growth investment | c. £25m transaction value; NVM 3.2x money multiple; 38% IRR; NVM retained 10% equity | CloserStill had grown from launch to a target £3m EBITDA, with ten major UK exhibitions and early international expansion. |

| 10 | Jan 2015 | Clarion Events | Providence Equity | VSS / Trilantic / shareholders | PE acquisition | Reported just over £200m | Providence enters Clarion, then exits to Blackstone in 2017. |

| 11 | Mar 2015 | CloserStill Media | Inflexion | Phoenix Equity Partners / existing shareholders | Minority / partnership capital | PE News: deal valued at more than £100m; later reports cite more than £100m / strong Phoenix return | Inflexion completes partnership capital investment; this is the real inflection point in CloserStill’s valuation arc before Providence’s later entry. |

| 12 | Mar–Jul 2015 | Comexposium | Charterhouse | Unibail-Rodamco / CCIR structure | Acquisition of c.50% / 50.1% stake | €550m implied Comexposium value | Charterhouse buys into one of the world’s largest exhibition organisers. |

| 13 | Apr 2017 | Emerald Expositions | Public markets, still Onex-backed | Onex-backed vehicle | IPO | 15.5m shares at $17/share = $263.5m gross offering size | PE-backed US exhibition platform accesses public markets; Onex retains control. |

| 14 | Jul 2017 | Clarion Events | Blackstone | Providence Equity | PE-to-PE sale | Reported £600m | Benchmark exhibitions PE-to-PE trade; around 3x Providence’s reported 2015 entry value. |

| 15 | Jan 2018 | UBM | Informa | Public shareholders | Strategic acquisition | £3.8bn cash-and-stock deal; combined group worth c. £8bn | Created a world-leading business events and exhibitions group; Reuters reported UBM had a 300-strong event portfolio and that the deal increased Informa’s events exposure from around 35% to almost 60% of group revenue. |

| 16 | 2018 | CloserStill Media | Providence Equity | Inflexion, NVM, management | Majority acquisition | Reported £340m | Providence buys CloserStill after Inflexion’s growth phase; Inflexion says the business expanded into Asia, Germany and the US, completed eight acquisitions, grew exhibitions by just under 50%, and increased international revenue from 20% to 50%. |

| 17 | Sep 2018 | Questex | MidOcean Partners | Shamrock Capital | PE acquisition | Reported c. $180m | MidOcean acquires Questex from Shamrock Capital as a hybrid B2B information, media and events platform in travel, hospitality, pharma, healthcare, beauty and technology. Flashes & Flames reported a c.$180m price, equal to 1.8x revenue, with Questex operating over 125 tradeshows and employing over 350 people across the US, Europe and Asia-Pacific. |

| 18 | Nov 2018–Mar 2019 | Comexposium | Crédit Agricole Assurances | Charterhouse | Sale of Charterhouse stake | €877m reported for Charterhouse stake; official completion undisclosed | Charterhouse exits to long-term institutional capital; Crédit Agricole Assurances becomes partner to the Paris Chamber. |

| 19 | Jan–Feb 2019 | Mack Brooks Exhibitions | Reed Exhibitions / RELX | Stephen Brooks / private owners | Strategic acquisition | Undisclosed officially; press reports c. £200m | Strategic sale of a founder-led B2B exhibition portfolio; relevant to Opus Origin’s founder-capital story. |

| 20 | May 2019 | Tarsus Group | Charterhouse | Public shareholders | Take-private | £561m equity value; £668m EV; c.17x average EBITDA | Defining listed-events take-private. |

| 21 | Aug 2019 | Hanson Wade | Graphite Capital | Management / founder-backed structure | Management buyout / PE acquisition | Reported £102m | Graphite backs the MBO of Hanson Wade, a conference organiser and information-services business focused primarily on pharma and biotech. Hanson Wade had almost doubled its events portfolio to 108 between 2016 and 2018, with revenue up 117% to £22.6m. The business also owned Beacon, a scientific data product, making this a useful early example of the events + data / information-services thesis. |

| 22 | Dec 2019 | ROAR Techmedia / ROAR B2B | Apiary Capital | Prysm portfolio / management-backed platform | PE-backed platform formation / acquisition | Undisclosed | Apiary backs ROAR as a lower-mid-market events platform around environment, healthcare and business technology. |

| 23 | Jul 2020 | Nineteen Group | Phoenix Equity Partners | Founder Peter Jones / existing shareholders | PE investment / growth capital + first acquisition | Reported c. £10m | Phoenix invests alongside founder and CEO Peter Jones and simultaneously backs Nineteen’s first acquisition, Western Business Exhibitions. Nineteen then owned International Security Expo and International Disaster Response Expo, together attracting 350+ exhibitors and 12,500 international decision-makers; Western added security, health & safety, fire and facilities management assets. |

| 24 | May 2021 | Arc Network | EagleTree Capital + Simon Foster-led consortium | New platform | PE-backed platform formation | Undisclosed | Explicit platform formation to acquire events, event groups and JVs with organisers, associations and venues. |

| 25 | Aug 2021–Oct 2022 | Arc Expansion | Arc / EagleTree | AgriBriefing, Fortem, Incisive portfolios, Bridge2Food, HighQuest, LRP assets | Buy-and-build / expansion | Undisclosed across announced acquisitions | Arc rapidly builds vertical clusters in agriculture, sustainability, HR tech, edtech, financial services and food. |

| 26 | 2022 | InfraXmedia / DCD platform | Opus Origin / Stephen Brooks-backed capital | DCD / digital infrastructure media-events base | Platform formation / acquisition base | DCD reported c. £10m revenue at time of majority acquisition | Opus Origin begins building an events/media/data platform in digital infrastructure. |

| 27 | Mar 2023 | Tarsus Group | Informa | Charterhouse | Strategic acquisition / PE exit | $940m initial enterprise value; c.9.9x post-synergy EV/EBITDA | Charterhouse exits to the largest strategic buyer in B2B events. |

| 28 | Jun 2023 | Hyve Group | Providence + Searchlight | Public shareholders | Take-private | c. £524m enterprise value; c. £363m equity value | Providence and Searchlight form the sponsor partnership later mirrored in CloserStill. |

| 29 | May–Jul 2024 | Easyfairs | Cobepa + Inflexion + founder Eric Everard | Founder-led structure | Strategic investment / partnership capital | Undisclosed officially; PE Hub reported over €600m transaction valuation | Founder-led organiser brings in PE capital for launches, geo-cloning, AI/data and M&A. |

| 30 | Sep 2024 | Nineteen Group | Phoenix continuation fund led by Kline Hill, co-led by Ares | Phoenix flagship fund | Continuation fund / recap | £200m continuation fund; EN reported c. £225m deal | Nineteen is held longer rather than sold, reflecting PE appetite to compound strong events platforms. |

| 31 | Nov 2024 | Quantum World Congress | Events Venture Group | QWC / Connected DMV structure | First EVG investment | Undisclosed | EVG appears as a new event-entrepreneur capital and mentorship vehicle. |

| 32 | May 2026 | CloserStill Media | Searchlight + Providence | Providence remains invested | Co-control recapitalisation / new investment | Reported £1.35bn / $1.77bn valuation; Searchlight co-control with Providence | Searchlight joins Providence rather than Providence selling outright; strongest current signal of PE conviction in B2B events. |

| 33 | May 2026 — announced / pending | Emerald + Questex | Apollo-managed funds | Onex / Emerald public shareholders; MidOcean / Questex | Announced take-private + PE-to-PE acquisition + platform combination | Emerald: official c.$1.5bn estimated closing EV; Questex undisclosed; AMO estimates Questex at a bit over $500m | Apollo intends to combine Emerald and Questex into a private North American B2B experiential events and media platform with approximately 160 events. |

| 34 | Jun 2026 — announced / pending | Hyve Group | Hellman & Friedman | Providence + Searchlight | PE-to-PE sale / secondary buyout | Reported about $1.8bn; price not officially disclosed | H&F buys Hyve after Providence and Searchlight’s 2023 take-private. FT reports Hyve reached $391mn revenue and $100mn EBITDA in 2025, with 15% organic revenue growth, 39% growth including acquisitions, and 26% EBITDA margins. H&F frames premium events as benefiting from the rising value of human connection in an AI-shaped market; treated as closed for dataset purposes. |

This table was built using publicly available sources and can contain inaccuracies. Reported values may refer to transaction value, enterprise value, equity value, gross IPO proceeds, stake value or press-reported valuation, depending on what was publicly available.

This table was built using publicly available sources and can contain inaccuracies, let me know if you’d like anything fixed.

Looking at this, a few eras emerge:

Setting the Scene: Events Become Investable - until 2013

Before the mega-deals, the groundwork was being laid. This was the period when private equity and strategic buyers started to carve out, professionalise, scale, and sell Events businesses.

The Long Growth Cycle: Platforms Get Re-rated - 2013 to Covid

Onex’s acquisition of Nielsen Expositions for $950m in 2013 was a major milestone. Suddenly, events were not just mid-market buyout opportunities. They were large-scale platforms. Then the pattern accelerated. Inflexion backed CloserStill. Charterhouse bought into Comexposium. Providence bought Clarion, then sold it to Blackstone. Providence later bought CloserStill. Charterhouse took Tarsus private. The strategic market also set a high bar. Informa’s £3.8bn acquisition of UBM in 2018 was not a PE deal, but it mattered. It showed what strategic scale in B2B events could look like. It also told PE owners that large event portfolios could attract serious strategic value when they had the right shape. This is where I spent most of my exec time during the ITE→Hyve transformation.

Covid Recalibration: The Industry Refuses to Die - 2020 to early 2023

All of a sudden, everything stopped. COVID was the ultimate stress test. Events businesses went from highly cash-generative to operationally frozen almost overnight. Venues closed. Calendars disappeared. Forecasting became guesswork. The industry entered uncharted waters. This could have broken the investment thesis.

- It did not -

The underlying customer need did not disappear. Buyers and sellers still needed markets. They still needed trust. They still needed discovery. They still needed commercially useful moments of concentration. I’ve argued before that business events are handshakes businesses; they compress trust, discovery, and commercial intent in ways that digital channels struggle to replicate on their own.

We’re So Back: Flip Assets Become Compounding Assets - 2023 to now

Informa’s acquisition of Tarsus from Charterhouse in 2023 was the moment the market really reopened. This deal told the market that large events platforms were back in play, and that strategics would still pay for the right assets. Providence and Searchlight took Hyve private. Cobepa and Inflexion recapitalised Easyfairs alongside founder Eric Everard. Phoenix moved Nineteen into a continuation fund rather than selling.

Then came the crazy 20 days at the end of Q2’26, where PE splashed £4.2bn to IRL (in-real-life)

CloserStillThis is where the story changed. The old model would have been simple: Providence sells, another fund buys, the asset moves on. Instead, Providence stayed in and brought in Searchlight, its co-investor from Hyve (then). Clearly, the smart money sees more upside in staying and compounding rather than cashing out and taking their money somewhere else.

Apollo / Emerald+Questex

By combining Emerald with Questex, Apollo is creating a much larger North American B2B events and media platform, with exhibitions, conferences, hosted-buyer formats, content, data, and year-round engagement sitting under one roof. That feels very aligned with where the market is going: not just bigger shows, but broader market-access platforms.

Whether Apollo turns this into another long hold remains to be seen. But the direction is clear. At the top end of the market, private capital is building larger, more durable platforms designed to compound over time.

Hyve

Providence and Searchlight did not stay in Hyve; they sold it to Hellman & Friedman for a reported c.$1.8bn. That looks like the old flip model at first glance. But the substance is different. Hyve was taken private in 2023, built aggressively through acquisitions, reportedly delivered $391m of revenue and $100m of EBITDA in 2025, and is now being bought by another large sponsor that clearly sees more road ahead.

So the flip is not dead. It has moved up a level. The buyer is no longer simply acquiring a portfolio of events. H&F is underwriting a premium platform in a market where human connection, trust, content, intelligence and year-round engagement are becoming more valuable, not less.

H&F's Hunter Philbrick called live events "one of the defining megatrends in the years ahead" as AI reshapes commerce. That framing isn't sentimental. I argued in 2020, at the bottom of Covid, when Zoom was the supposed F2F-killer, that face-to-face beats every other mode of B2B interaction on three things: trust building, complex problem solving, and speed of solution. COVID was the first stress test of whether those three were real or industry mythology. AI is the second. Buyers like H&F and Apollo are underwriting them as structurally more valuable, whilst synthetic content floods every other channel.

Let’s have a look at these patterns in detail:

Major announced deals, 2004–2026. Log scale. Bubble area is proportional to reported value. Coloured arrows connect repeat ownership of the same asset. Numbers refer to the source-table row.

Note on the mutual exit (#33): Apollo’s announced combination of Emerald and Questex is the end point of two separate ownership tracks — Onex’s Emerald hold (#8 → #13 → #33, dashed, since the 2017 IPO was a non-control event) and MidOcean’s Questex hold (#17 → #33). The 2026 figure is a working assumption for the announced deal (Emerald c. $1.5bn EV + Questex est. c. $500m; completion expected H2 2026).

Platform formations and still-undisclosed deals (Comexposium formation, ROAR, Arc, Opus Origin / DCD, Quantum World Congress) are omitted from the plot. Values shown as reported (transaction value, equity value or enterprise value as available); currency conversions are approximate at period rates. Sources: company filings, Reuters, FT, the Guardian, Conference News, Exhibition News, Flashes & Flames, PE Hub, TSNN, Buyouts Insider, Charterhouse, Inflexion, Phoenix, Searchlight, Informa, Apollo, Emerald investor communications.

Sincere thanks to my brilliant assistant, Claude, who put this visualisation together.

In the beginning, events were carve-out opportunities. Then they became professionalised platforms. Covid tested whether the thesis was real. Now the strongest assets are being treated as compounding platforms, all while the next generation is being assembled underneath that story, through Arc, ROAR, Opus Origin, and EVG.

From flip assets to keep assets

A closer look at the CloserStill arc proves a change of direction: Phoenix (2014) → Inflexion (2015) → Providence (2018), and they were clearly heading for a fourth flip. But May 2026 broke the pattern: Providence didn't sell out, Searchlight came in alongside at a £1.35bn / $1.77bn valuation. That's a co-control recapitalisation, not an exit. Same fund stays in the asset, brings a partner, takes some chips off, holds for the next leg. Searchlight's own messaging ("alongside Providence... next phase of growth") explicitly markets the partnership rather than the handover.

This is the structural shift. And it's not isolated:

Nineteen Group, Sept 2024: Phoenix moved it into a £200m continuation fund (Kline Hill, Ares co-leading) rather than selling. Same logic, keep the platform, recycle LP capital.

Comexposium, 2018–19: Charterhouse exited not to another PE fund but to Crédit Agricole Assurances. Insurance capital is functionally a buy-and-hold owner.

Easyfairs, 2024: Cobepa (a Belgian holding company, not a closed-end fund) plus Inflexion took shares alongside founder Eric Everard. Long-dated capital, not a flip vehicle.

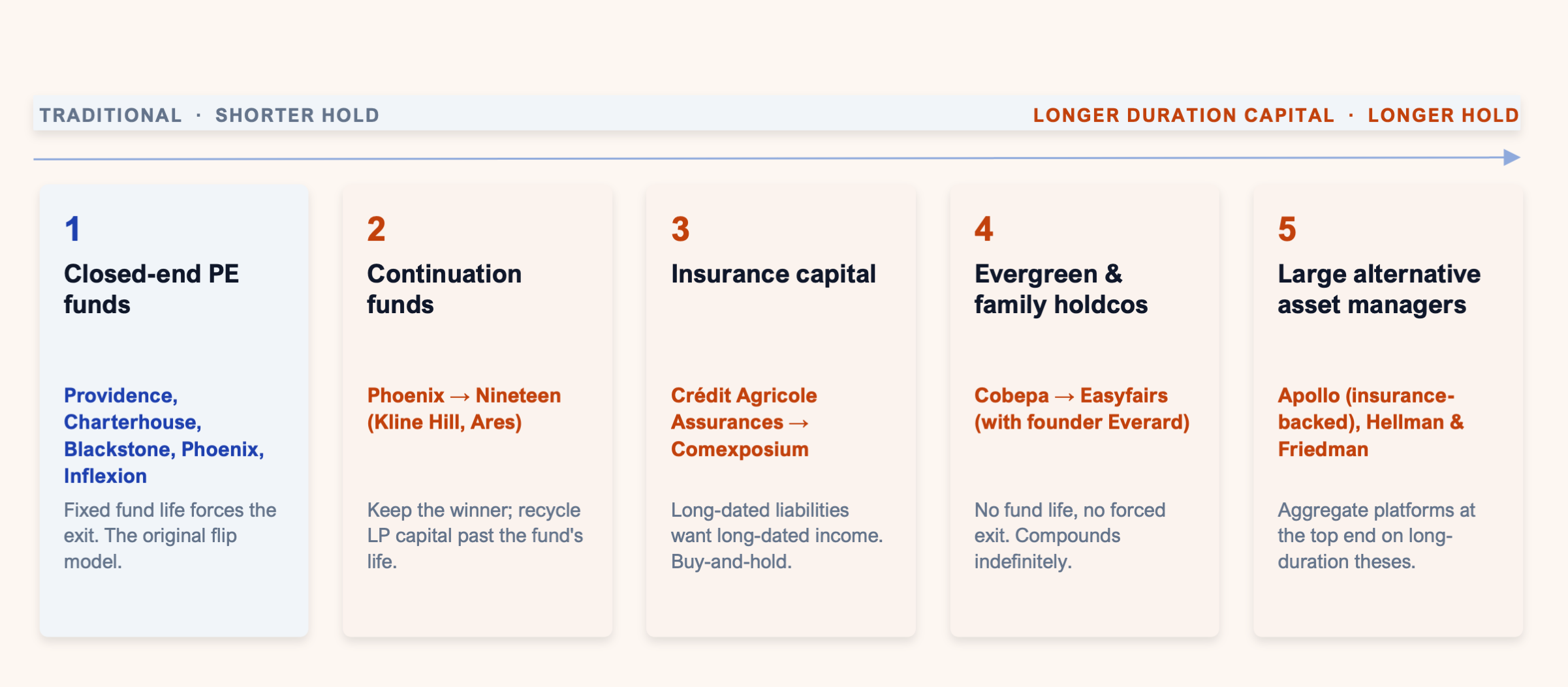

So three different mechanisms, continuation funds, insurance balance sheets, and evergreen holdcos are all converging on the same thing: keeping good event platforms in the same hands for longer. But the deeper point underneath all three is that the capital changed, not just the strategy. For most of the last two decades, the buyer at the top end of events was a closed-end PE fund (Providence, Charterhouse, Blackstone, Phoenix, Inflexion), and a closed-end fund runs on a clock: a fixed life that eventually forces a sale, whether or not the asset has finished compounding. That clock is what produced the flip model in the first place; it was never really a verdict on the business, just the shape of the capital that happened to own it.

What's changed since Covid is that events now draw capital that doesn't run on that clock. It sits along a spectrum, from the traditional, shorter-hold fund at one end to genuinely long-duration capital at the other: continuation vehicles, insurance balance sheets, evergreen and family holdcos, and now, at the very top, the large alternative asset managers, Apollo with its insurance-backed capital and Hellman & Friedman with its long-duration growth thesis.

Five years ago, this mix of capital was barely visible at the top end of B2B events. Today, it is defining the exit market. CloserStill is the most visible because of the headline number, but it's the trend, not the exception: the clock didn't disappear, the capital that owns events simply stopped running on a five-year one.

Average PE ownership tenure by year

Average tenure of selected PE / PE-style events ownership cycles by exit, continuation or recap year, with a 3-deal rolling average calculated on the underlying ownership-cycle sequence.

Notes: tenure is calculated from PE / PE-style entry to exit, continuation fund, or recapitalisation event. Nineteen / Phoenix is now calculated from Phoenix’s July 2020 investment to the September 2024 continuation fund, giving c.4.2 years. Emerald / Onex, Questex / MidOcean and Hyve / Providence + Searchlight are treated as closed in 2026 for tenure illustration. The rolling average is calculated on the underlying ownership-cycle sequence and shown once per year using the year-end value. Durations are approximate and rounded to one decimal place.

The chart above solidifies that story. Across the disclosed PE ownership cycles in this dataset, average tenure at exit or recap has gone from around three and a half years in the mid-2010s to closer to eight since 2023. The post-2023 cohort runs longer at every data point: Charterhouse's exit from Tarsus at 3.8 years, Phoenix's continuation fund on Nineteen at around 4.2, and the new CloserStill recapitalisation at roughly 7.5 years and counting for Providence, whereas the Onex-Emerald ownership can be treated as an almost thirteen-year long-hold.

Hyve breaks the mould with a three-year hold by Providence and Searchlight, but hey, breaking moulds is what they do for a living.

The chart, by definition, only includes cycles that have already produced an exit, a continuation fund, or a recap. The longest current PE hold in B2B events doesn't appear on it: Blackstone has owned Clarion since July 2017, which is now into a ninth year. Easyfairs (Cobepa and Inflexion, 2024) is excluded for the same reason. In other words, the trend visible in the data is being held back by what's invisible to it: deals that have already been held longer than any dot on the chart, but haven't "completed" in a form the dataset can capture. The structural shift toward longer holds is real, and the chart, if anything, understates it.

PE ownership hold duration in B2B events

Approximate hold duration of selected PE / PE-style investments in B2B events and exhibitions. Includes completed exits, recapitalisations and ongoing holds.

Notes: durations are approximate and calculated to June 2026 where holdings are ongoing. Hanson Wade / Graphite is included as an ongoing hold from August 2019, giving c.6.8 years. Nineteen / Phoenix is calculated from Phoenix’s July 2020 investment to the September 2024 continuation fund, giving c.4.2 years. Emerald / Onex, Questex / MidOcean and Hyve / Providence + Searchlight are treated as closed for tenure illustration. Ongoing holds are shown in lighter blue. The orange vertical line shows the average duration across the displayed cycles.

The all-time average PE hold duration across the displayed dataset stands at c.5.3 years. Several ongoing hold assets sit above that line, including Clarion, CloserStill (through a new fund within Providence), Comexposium, Hanson Wade, and ROAR. The point is not that every individual asset position is meaningful in isolation; it is that long-duration ownership is no longer an exception at the top end of B2B events. It is now part of the ownership toolkit.

The Hyve sale to H&F looks at first like a counter-example. Providence + Searchlight held for only three years, far shorter than the rest of the 2026 cohort. But notice who's doing what. Providence + Searchlight are also the buyers staying in CloserStill at the same moment. They aren't choosing "flip vs hold" across the portfolio; they're rotating capital out of one platform to free up conviction for another. On the buyer side, H&F is explicitly underwriting a long-duration "human-connection megatrend" thesis. So even what looks like a flip is in fact selling into a hold. The pattern isn't every owner becoming a long-hold owner. It's every owner, even short-hold sellers, operating as if the asset class is now a compounding one.

The Strategic Exit Bottleneck

At the other end of the buyer spectrum, Informa sits almost alone. The UBM 2018 (£3.8bn) and Tarsus 2023 ($940m EV) deals top these charts for a reason. Informa is the only buyer big enough to absorb assets at PE-prime exit prices, softened by significant “synergies” and turn them into balance-sheet earnings. Reed/RELX bought Mack Brooks in 2019 (~£200m) but has been quiet since.

As we all know, there isn't a third strategic player of comparable appetite or size. Which means: PE owners selling at the upper end of the size curve have one realistic strategic exit, and that creates pressure to do something other than wait for Informa to call. Co-control deals and continuation funds can partly be seen as a response to that thin strategic bid. (Who’d go for an IPO these days?)

But the Apollo / Emerald + Questex announcement and the H&F Hyve deal together represent c. $3.8bn of PE-prime events assets clearing in a single month, neither of them going to a strategic buyer. Large alternative asset managers, Apollo with its insurance-backed capital, H&F with a long-duration growth thesis, are now a third realistic exit route at the top end, alongside Informa and continuation-fund / co-control structures.

What does the future hold?

The best platforms are becoming too valuable, too scarce, and too compounding to be treated as simple pass-the-parcel assets. With only a thin strategic buyer universe at the top end, and with organic growth, M&A, data, digital products, and year-round communities still underdeveloped across much of the sector, the smartest capital is choosing to stay closer for longer.

The new question for event owners is no longer simply “who buys next?” It is:

Who has the patience, structure, and conviction to keep compounding?

I spent most of Era II, “The long growth cycle”, working as an executive sponsor of multiple workgroups on the ITE→Hyve transformation: the £300M Ascential Events acquisition and integration, and the TAG Transformation programme. If you're a PE executive or a CEO inside one of these compounding holds, the value-creation work you need: pricing discipline, rebook architecture, data, digital, M&A integration, is exactly what I help with. Not strategy decks. Operating sprints, with board-level reporting. Let’s have a quick chat, or simply send me an email.

Alternatively, The Event Strategy Bot covers the first mile of my thinking for free if you'd rather start there.

Further reading

If this topic is useful, these earlier pieces explore the same themes from different angles:

Are we in a seller’s market? And is Private Equity to blame? — on post-COVID growth, acquisition pressure, and the return of inorganic growth.

Is the events industry (really) consolidating? — on market concentration and why the industry remains more fragmented than many assume.

Digital Self Assessment for Media and Events CEOs— on the digital and data questions boards should be asking.

A comparative study on B2B interaction — a foundational article on the power of Face-to-Face communication.

Article updated on 9th of June 2026